In 2016, the aggregate payment was born, and suddenly, for a time, the aggregation payment was all over the world, and the rumors of aggregate payment were everywhere, and it was familiar! So, what exactly is the aggregate payment?

On Baidu Encyclopedia, aggregate payment is also called convergent payment, aggregation is good, integration is also worth mentioning, literally, as the name suggests, is to put together the payment together.

Payment is an indispensable part of life and a key part of the closed-loop business model.

In the traditional era, payment scenarios were concentrated online. In addition to cash, merchants mainly collect money through POS card swiping, and the payment institutions are mainly banks and three-party payment companies.

In the Internet era, online shopping has taken off, and third parties to the Internet have paid for Alipay and Tenpay.

Nowadays, stepping into the era of mobile Internet, mobile phone payment: Alipay, WeChat payment has become a darling.

But the problem is coming...

In the era of mobile Internet, traditional offline, Internet, mobile Internet, triple space scenes exist at the same time, superimposed on each other.

Consumers are also distributed in the offline, PC and mobile phone portals.

The business scenarios of the business model are endless, constantly cross-border, and the payment scenarios involved are also fragmented.

Merchants need to provide consumers with a full-scenario, all-in-one payment collection service.

In terms of supply, the industry structure and supply chain of payment, in terms of links and services, are insufficient to cope with such intricate and sudden changes.

Ok, who is the target of the payment needs?

Different payment officials provide their own payment methods, provide standardized interfaces, and provide standard answers for customer service. ...the result, you know...

Therefore, the aggregate payment came out.

It is the era that has spawned aggregate payment, which is a fragmented mobile Internet era payment scenario. The objective existence of payment demand has spawned aggregate payment.

In other words, Aggregate Payment is the solution to pay for the mobile Internet era! It is the solution generated by the systematic automatic evolution of payment!

Therefore, the aggregation payment will be fire, which is self-evident, and it is a matter of course.

Aggregate payment is a structured payment service solution in the mobile Internet era!

The so-called aggregate payment is to rely on the payment channel and clearing ability of the bank, three-party payment or clearing organization to provide customers with payment, service, interface, integration, docking, order processing, data statistics and other payment service agencies.

By syndicating the paid SDK, aggregating payment scenarios, aggregating payment methods, and aggregating payment channels, there is no need to find a desired payment channel, no need to repeatedly connect and integrate cumbersome payment interfaces, link merchants and channels, reduce access technologies, communicate thresholds, and lower Channel cost, convenient and fast access to pay.

In the era of mobile Internet, the scene of docking of mobile payment is more fragmented and has superior timeliness.

The inability to easily connect with customer needs and the inability to implement services quickly means giving up customers. The era needs to aggregate payment as a payment institution to realize the rapid landing of mobile payment!

Related Links

96 fee reform policy

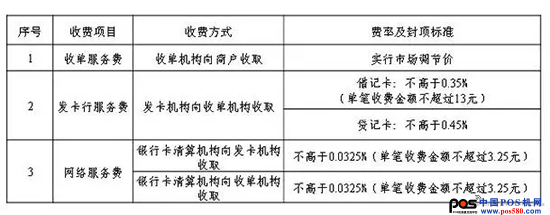

In the "Notice on Improving the Pricing Mechanism for Bank Card Credit Cards" jointly issued by the National Development and Reform Commission and the People's Bank of China, the service fees for the more adequately charged acquisitions are changed from the current government guidance price to the market adjustment price, and the acquiring institution and The merchant negotiates to determine the specific rate. The fee change has been officially implemented since September 6, 2016.

1. After the 96 fee is changed, the bank card processing fee and the upper limit of the rate

2. The distribution mechanism of the acquirer before and after the 96 fee change

The central bank pays for the name of the aggregate and encourages the development of aggregate payments!

[2017] No. 45 document "Guiding Opinions on Continuously Improving the Level of Receiving Service, Standardizing and Promoting the Development of the Receiving Service Market" clearly stipulates that the encouragement of aggregate payment is given, and the value of the aggregate payment to the merchant is clearly affirmed.

Network Alliance starts operation

On March 31, the non-bank payment institution's online payment clearing platform (hereinafter referred to as the “networking platformâ€) started the trial operation, and the first batch of access to some banks and payment institutions. Payment under the UnionPay extension cable, "network connection" transfer online payment, third-party payment platform can choose to access one of them, but can not continue to directly connect to the bank mode.

The payment agency's reserve fund centralized deposit management began to implement

According to the Notice of the Central Bank of China on January 13, the Notice of the General Office of the People's Bank of China on Implementing the Central Depository of Deposits for Customers of Payment Organizations (Yin Ban Fa [2017] No. 10) (hereinafter referred to as Document No. 10), from 2017 From April 17 of the year, the payment institution shall deposit the customer's reserve fund to a designated institution's special deposit account according to a certain percentage. The average ratio of first deposits required by the document is around 20%. In the future, the bank will no longer pay interest on the provision for centralized depository.

Hair Removing Machine,Ipl Hair Remover Machine,Hair Laser Removal Machine,Ipl Laser Hair Removal Machine

Guangzhou Lesen Xinpin Electronics Co.,Ltd , https://www.lesenxinpin.com