The trend of strengthening the supervision of the mutual gold industry in 2016 will continue in 2017. After the third-party payment institution was required to implement the bank's three-party depository, the “fourth party†payment institution – the area of ​​aggregate payment – ​​also joined the bank's rectification queue.

On the eve of the Spring Festival, the Central Bank issued a notice to its branches on the cleanup and rectification of illegal “aggregate payment†services. Although the central bank’s actions were very low-key, the notice spread quickly in the industry. .

According to the notice, the regulatory authorities require the inspection and management of the “aggregate payment†service agencies and their businesses in all jurisdictions to be completed before February 28, 2017. Subsequently, various media outlets successively published the original notices issued by regional branches such as Jinan and Shenzhen, and there were many regulators around the country who “encircled and encircled†the aggregate payment.

So, what is the aggregation payment? How does the aggregation payment step on the regulator's mine?

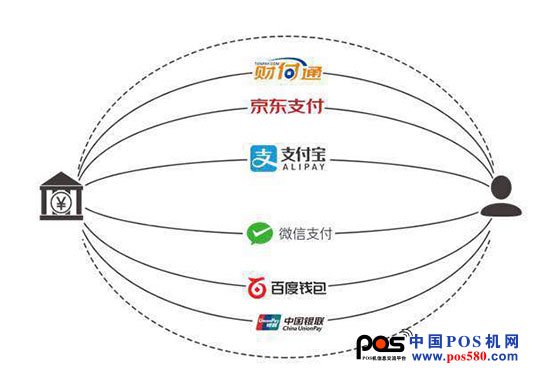

Aggregate payment service is a payment channel and clearing settlement capability based on commercial banks, non-bank payment institutions, national/regional clearing organizations, etc., and integrates payment services of these institutions with their own technology and service integration capabilities. Within the scope of the regulation, the merchant provides various payment services such as technical docking, collective reconciliation, and error handling.

Generally speaking, aggregate payment is a technical service that aggregates many third-party payments to provide merchants with convenient payment and saves the cost of cash. As the size of the third-party mobile market expands, payment institutions are increasingly fragmented, in which case they can simplify the payment process and provide merchants with a range of services for the aggregation payment market.

Standardized aggregate payment can effectively help merchants to reduce payment costs, improve merchants' payment efficiency, and optimize the merchant's payment experience. However, the premise of this benefit is standardization. When this payment method breaks away from the boundary of compliance, a series of chaos of violation of law and discipline arises.

The "Notice" issued by the central bank mentioned that

"Aggregation technology service providers are strictly positioned in the outsourcing agency, and must not engage in merchant qualification review, acceptance agreement signing, fund settlement, acquiring business transaction processing, risk monitoring, acceptance terminal (network payment interface) master key generation and management, error Core business such as dispute resolution; may not settle funds in any form by special merchants, engage in or disguise in the settlement of special merchant funds; may not forge, falsify or conceal transaction information; may not collect or retain sensitive information of special merchants and consumers..."

The four “not allowed†are the “minefields†that some of the current illegal technology service providers have stepped on. These service providers have thus become the "second Qing institutions" that everyone is calling.

There are many types of aggregation payment service providers, including technology integration, institutional transfer, institutional direct clearing, and capital clearing. The technology integration class provides technical docking services for merchants. The agency transfer class engages in information aggregation services through qualified institutions. The organization is directly responsible for qualified organizations to make aggregate payments. These three types of aggregate payment services are legal and compliant. . The only type of “funding and clearing classâ€, which does not have the corresponding qualifications but is engaged in payment business and fund clearing work, is the main target of the central bank.

Since the central bank issued payment licenses, as of now, there are more than 200 third-party companies that have issued non-financial institutions issued by the People's Bank of China, and only 62 of them have bank card acquiring licenses, including national acquiring licenses. Only 43. Among the only dozen companies that have the ability to receive orders, only a few large third-party payment institutions, including Alipay and WeChat, have competitive advantages. Therefore, on the one hand, service organizations that do not have the qualification for fund clearing want to gain a share in this market. On the other hand, small payment companies suppressed by monopolistic third-party payment institutions choose to outsource their services to aggregate payment services. Business has caused the industry chaos in the field of mobile payment, which is full of “Second Qing institutionsâ€.

Erqing institutions have running risks

It is not uncommon for the risk of the second clearing POS not being accounted for and the merchant’s purchase price to be falsified into other people’s accounts. A formal aggregation payment service provider should only participate in information processing and not touch the liquidation of funds. However, in the second clear mode, the transaction funds enter the account of the agent before clearing to the merchant, and only when the merchant takes the initiative to withdraw, the funds can be In the hands of the business. Usually, the merchant's collection time is in the form of T+1. If the funds are in the hands of the aggregate payment service provider, a deposit will be formed. Similar to the P2P platform with a pool of funds, the cost of running the organization is greatly reduced.

According to a report by a central bank official, "if purely technical integration does not involve the precipitation of funds and sensitive customer information, it is a relatively standardized aggregate payment; but once the funds are involved, it must be stopped immediately, and supervision must be promptly involved. It is impossible to repeat the previous passive situation of third-party payment institutions." When the aggregation payment institution can access the client's funds, it must be alert to the risk of misappropriation.

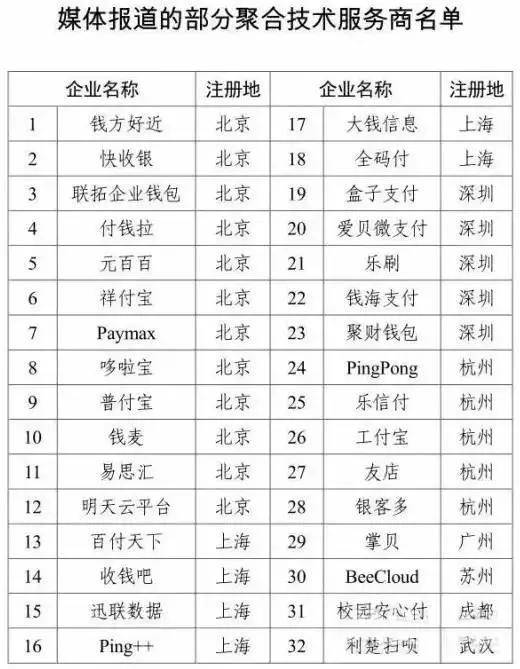

The list of central bank announcements is accompanied by a list of “partial aggregation technology service providersâ€, including 32 domestic aggregation payment companies. Some of these companies may focus on technology, but some service providers cannot be excluded. There is a suspicion of "two clears."

The profit model of aggregate payment is still being explored

The unclear profit model has indirectly led to the emergence of the “two clear phenomenonâ€, and it is more profitable to make fund clearing than to charge a meager handling fee. Therefore, developing more application scenarios for aggregate payment will be the main development direction of the industry.

The aggregate payment service is mainly divided into online business and offline business. Offline is an aggregate payment receipt, which collects the receipts of different payment methods in one QR code or one terminal, mainly for physical store services. Online is the aggregation of network payments, integrating various payment methods (WeChat, Alipay, etc.) into their own platforms, mainly for e-commerce services.

At present, there have been more than 30 aggregate payment service agencies in China. In addition to charging traditional trading service commissions, these companies are exploring how to use technology to generate more service revenue. For example, a consumer finance scenario is derived, and advertising is used to generate revenue. For example, the aggregate payment service provider Qianyuan is close, and launched the first consumer community based on the office building business circle to serve office workers and merchants. Ping++ focuses on using technology to improve services, exploring new charging models, and perhaps coming out of a new path that is different from fees.

The first shot of the central bank’s choice to rectify the aggregation payment industry at the beginning of the new year is bound to serve as a deterrent to the Erqing institutions on the market. Strict supervision will not affect the development of the entire industry. On the contrary, after a new round of inventory, the good money in the market may be able to drive out the bad money and drive the healthier development of the whole industry.

Silicone Soap Holder

SELF-DRAINING DESIGN - KEEP DRY: The soap dish for adopts waterfall self-draining structure, so it can drain quickly. Stop Mushy Soap, Keeping the soap dry and the countertop clean.

SILICONE MATERIAL - SAFE AND DURABLE: The bar soap holder is made of high quality silicone material, no plastic, soft in texture, skin-friendly touch, safe and non-toxic, heat resistant, no color change, no breaking.

ANTI-MELTING & ANTI-SLIP DESIGN: The four raised stripes on the front prevent the water from contacting the soap and 100% protect the soap from melting. The four non-slip corners at the bottom effectively prevent the soap saver from slipping.

YDS Product categories of Silicone Household Supplies, we are specialized manufacturers from China, Silicone Cup Coaster , Silicone Placemat , Silicone Drinking Top , Silicone Gloves , Silicone Cake Mold ,Silicone Ice Cube Tray, Silicone Wine Cup , Silicone Identifier ,Silicone Bottle Stopper , Silicone Door Stopper ,Silicone Soap Holder, Silicone Shoe Covers , Silicone Straw ,Silicone Foot Cover & Protector,Silicone Cigarette Holder Clip ... Our Factory Advantages:

1.Mold workshop and 2D and 3D engineer department

2.Solid siliccone compression machine and liquid silicone injection machine

3.Disney and Sedex 4P audit factory

4.ISO 9001,IATF16949,Raw material of FDA LFGB MSDS Certificates

1.Mold workshop and 2D and 3D engineer department

2.Solid siliccone compression machine and liquid silicone injection machine

3.Disney and Sedex 4P audit factory

4.ISO 9001,IATF16949,Raw material of FDA LFGB MSDS Certificates

Look forward to your cooperation!Soap Container,Silicone Sponge Holder,Sink Organizer Tray,Kitchen Soap Tray Sponge Holder

Shenzhen Yindingsheng Technology Co., Ltd , https://www.dgoemsiliconeyds.com